Rate Buy Downs- What is it?

Jennifer Martin September 5, 2023

Jennifer Martin September 5, 2023

Jennifer Martin September 5, 2023

Rate Buy Down- what is it, why would you use it, how much does it cost, what does it save you, who pays for it?

In this article we'll break down each of these questions so that you can decide if it is the right program for you, whether you are a thinking of buying or selling a home.

Before we dive into buy downs, first, you need to understand how loan pricing works. Lenders are sent daily rate sheets from the banks that give them their money, to give to you. Each day they find out what the going rate is to be at or close to "par." Par rate means that it doesn't cost any extra fees to get that rate. Some lenders are required to lend at a certain price. Their branch or company may require a .25% pricing for example, so the lowest rate that they can lock at pays them .25% of the loan amount. This is fully dependent on each lender, their bank and the specific loan officer.

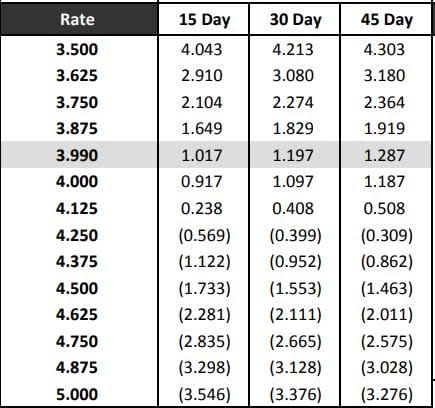

To learn about loan pricing, we are going to use the example rate and pricing sheet below. The columns are:

"Rate" the interest rate that the lender is able to quote, "15 day" means locking (or guaranteeing) that specific rate for 15 days, "30 days" it is locked for 30, and "45 day" it is locked or guaranteed for 45 days. You'll see that it "costs" more in points (percentages of the loan amount) to lock a loan for longer, because there is more risk and volatility in the rate markets over a longer period of time, so to hedge that risk, lenders charge more to lock for longer. ( Again, locking your rate means that the lender will guarantee you that rate on your mortgage as long as you close within that set number of days). The numbers in the rate columns underneath the lock terms are how much it costs in loan fees to get that rate guarantee for that number of days. If the number is in (parenthesis) it means that instead of a loan fee or cost, the buyer would get a credit from the lender for locking in at that higher rate.

In the above rate sheet, 4.25%, locked for 15 days has a credit of .569%, and 4.125 costs .238. If you had a 500k loan amount and locked in 4.25% for 15 days, there would be a lender credit of $2845. The lender may pass that on to you as the borrower, or they may keep it as additional income. For a rate of 4.125 at 15 days, there would be a loan cost of $1190, so to get that rate you'd have to pay an additional $1190 at closing as a loan cost or "discount point" in order to lock in that rate.

Historically, when rates were this low, one way to reduce the cash that a buyer needed to close, was to increase their rate by .125 or .25 or more, and to use the credit generated as a closing cost credit. In the scenario above, if a buyer was $2500 short on funds to close, or wanted to keep more money in their account and were ok with a slightly higher rate, they could take the 4.25% and have a $2845 lender credit at closing to offset closing costs. There are limits on how high you can go on this because conforming loans have limits on how much of the down payment needs to be your own funds (and this doesn't count). So you couldn't raise it super high and get 50K back at closing for example- but you could do it for small amounts to help with closing costs.

Now that interest rates are higher, buyers and sellers are considering the same manipulation of rates for credits- but in the opposite direction. Instead of raising the rate to bring less cash to close, some buyers are opting to bring MORE cash to close to "buy" their rate down. Buyers may opt to pay 1%, 2% in points to get their rate down. Why would they do this? Let's look at some amortization tables to figure out why and if it is a good idea.

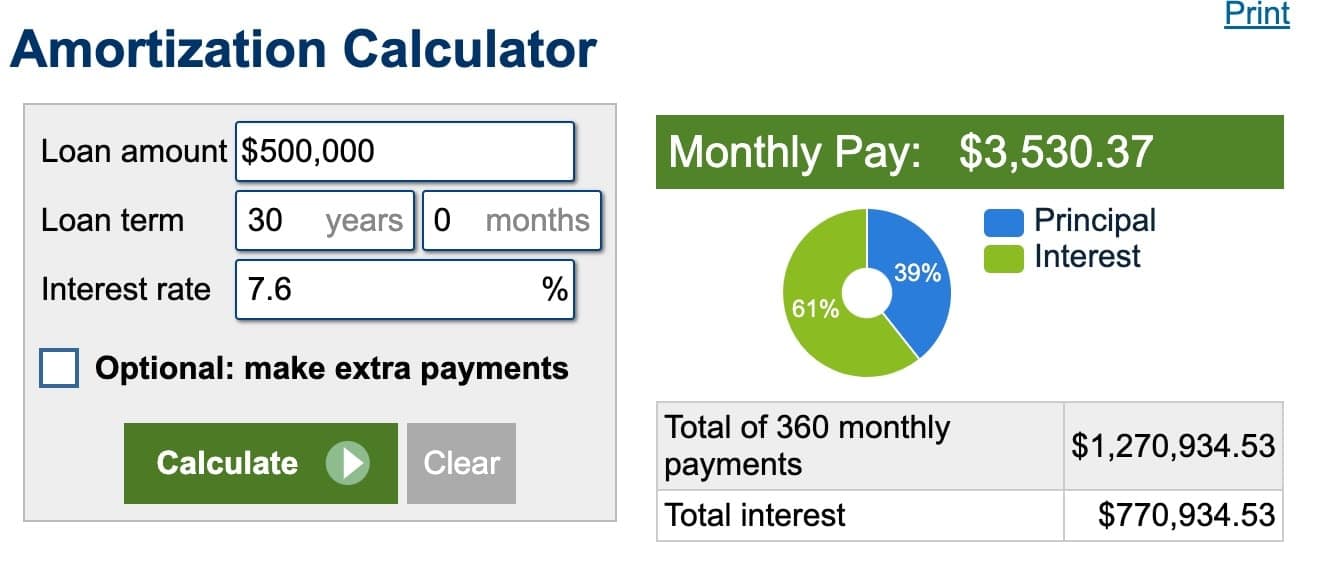

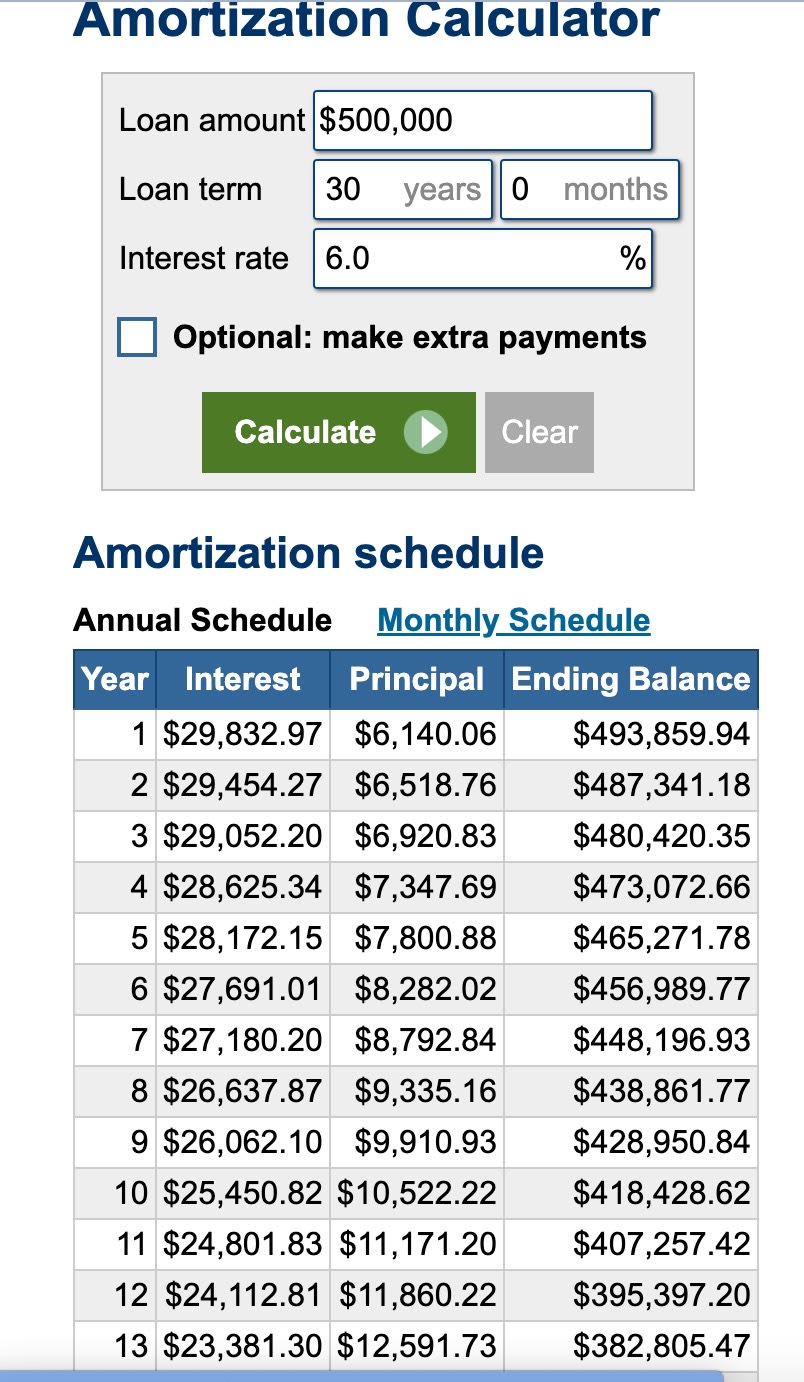

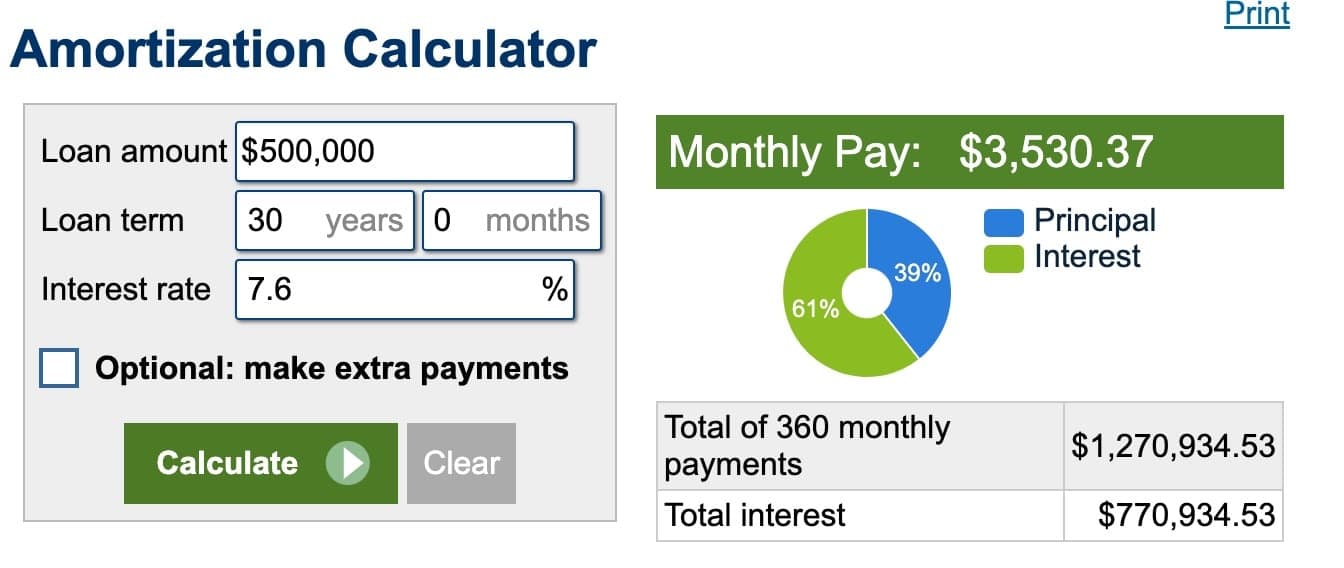

^ A 500K loan at 7.6% has a monthly payment of $3530.37. ^

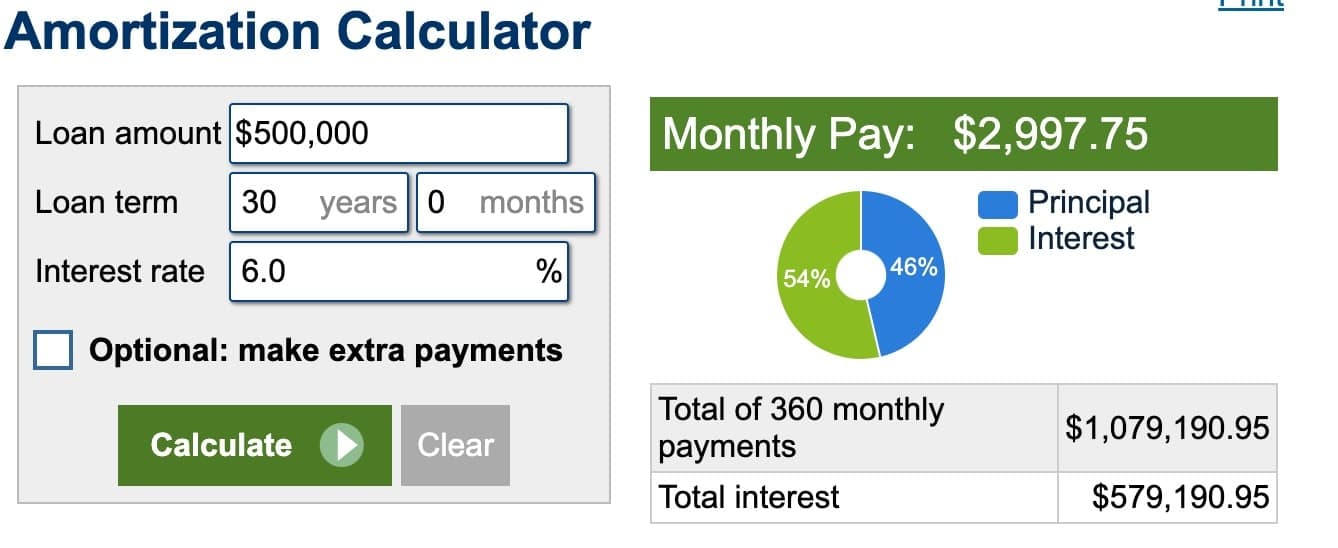

The same loan at 6% has a payment of $2997.50 for a difference in $532.87 per month. That can be a very significant difference for a buyer.

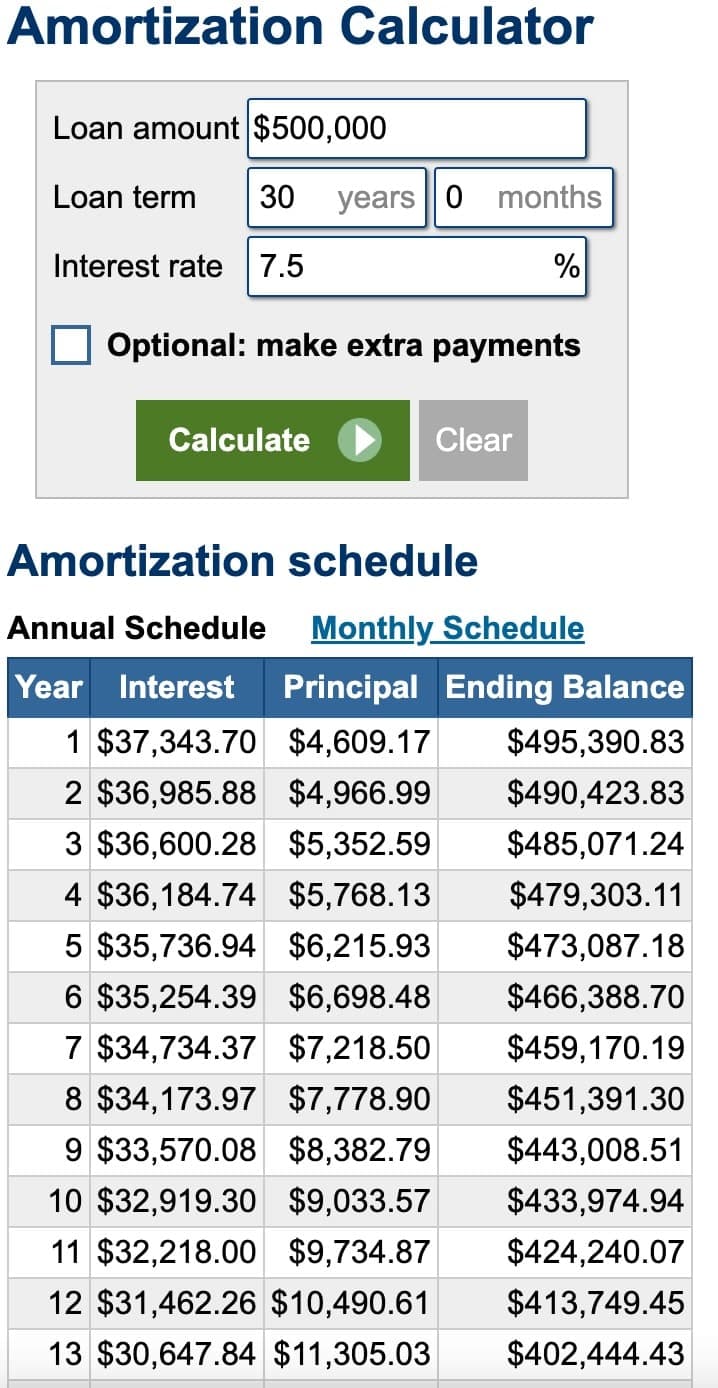

What if buying the rate down from 7.6% to 6% cost 30K? How would you know if that was worth the cost? For that answer we head back to the amortization calculator:

Comparing these two charts, if you look at the interest paid annually at the two rates, there is a difference in annual interest of $7510.73 in the first year alone. (Year 1 interest chart 1 - Year 1 interest chart 2). Keep finding the difference down the years and adding them together until you get to 30K. In this scenario it would take about 4 years to break even. If you are planning to live in the home for longer than 4 years, then it would make sense to do. If you are only planning to own the property for a couple of years then it may not make much sense to do at that amount. You could also figure out how long you are going to own the property and work backward to determine how much of a rate buy down makes sense.

Now on a seller side, why would a seller offer to pay this fee on behalf of the buyer? There are a few reasons that it would make sense for a seller..

When you list your home and there is plenty of a supply of homes for buyers to choose from, it is important that your home stands out from the crowd. Optimally this would be in amenities, aesthetics, location or price, but if you live in a pretty homogeneous area where homes are very similar, you'll need to be more creative in order to attract the right buyer. If you can offer your home at a significantly lower monthly payment than your neighbor's house, then you very well may win over the competition.

How much of a difference does it make and why would you not just reduce your sales price?

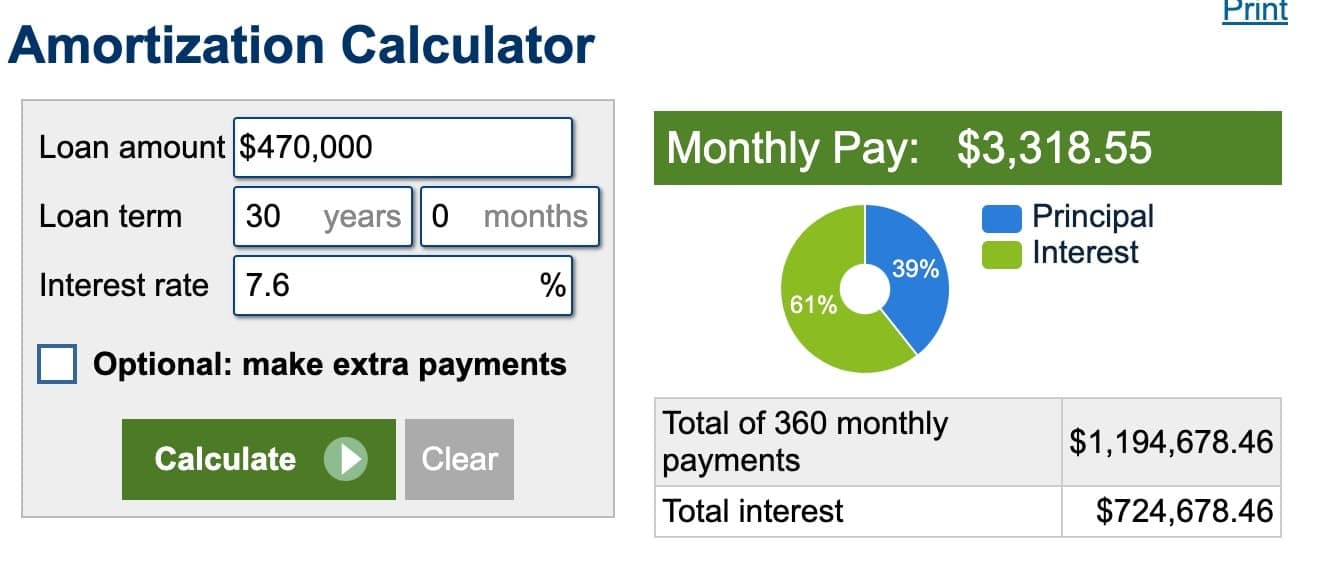

Let's look, using the 500K sales price and 30K seller concession amount in the earlier example.

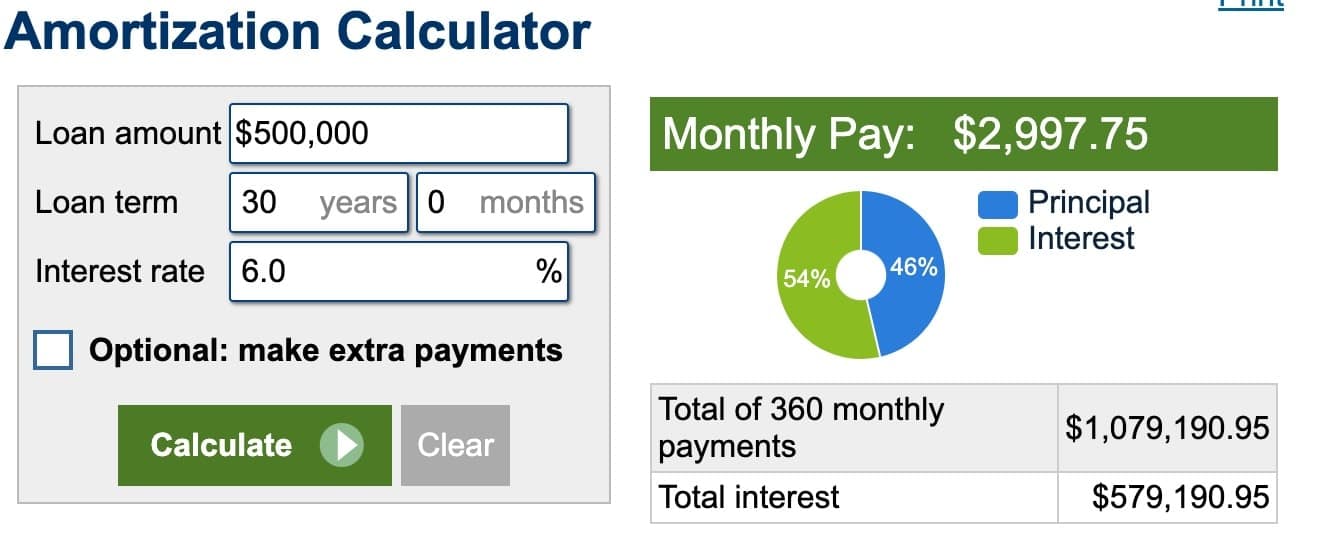

If, as a seller, you are offering 30K to a buyer, which makes a bigger difference, reducing the sales price to 470K, or buying their rate down to 6%? We go back to the chart!

A full price offer with a full price rate would have the buyer's payment at $3530.37/month.

If you take 30K off of the 500K sales price and the buyer still has a 7.6% interest rate, they have a payment of $3318.55 for a savings of $211.82/month.

If you take that same 30K and buy their rate down to 6%, the payment is reduced to $2997.75 for a difference of $523.62. That same 30k seller credit more than doubles the benefit to the buyer if used to buy the rate down vs reducing the purchase price.

Buying your interest rate down, or buying the rate down on behalf of a potential buyer on your home can be a long term money saving plan. There are some limits on how much you can buy it down, and there is a tipping point on which it no longer makes financial sense, but using a simple calculator you can determine if it makes sense for you!

Stay up to date on the latest real estate trends.

Defense Tech Leading the Hiring

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact Jen today.